Tuesday, June 30, 2009

Have Obama and the Democrats finally found someone they won't bail out?

As Time, Newsweek, the New York Times, and the rest of the news-in-print industry shrivels up, The Economist thrives.

Will

The story of the creation of the Prius.

Papists take over the Supreme Court. If Sotomayor is confirmed, six of the nine Justices will be Catholics under the control of Rome: Sonia plus Alito, Kennedy, Scalia, Thomas, and Chief Justice Roberts. They warned us that if John Kennedy was elected President this would happen, yet hardly anybody has noticed. The Pope operates in insidious ways.

Monday, June 29, 2009

Keynes did not support deficit spending to support the economy. Ever. At least if one can believe the Palgrave encyclopedia of economics [1998 edition] ...

"Despite the fact that the economics of deficit finance began with the Keynesian Revolution, it has been conclusively established by Kregel (1985) that Keynes himself did not ever directly recommend government deficits as a tool of stabilization policy. Keynes played a conservative political hand and viewed budget deficits with a 'clearly enunciated lack of enthusiasm'."Keynes advocated government spending in some circumstances to strengthen an economy -- but not deficit spending. Noted previously here was the fact that in 1937, when the unemployment rate in Britian was 11%, he opposed a government spending stimulus program.

What happened? Some of Keynes' first-generation disciples observed that the calendar year is an arbitrary time period for judging "budget balance" and concluded, not entirely unreasonably, that using the full length of the business cycle would be better -- so a deficit during one stretch of a multi-year cycle would be offset by surpluses during others, creating balance overall.

Then Keynes's second-generation disciples came along...

Sunday, June 28, 2009

More than $65 million a year...

637 AT SCHOOLS GET 'IDLE'-IZEDFor any who may wonder how this can be, a former NYC public school teacher explained how the entire sorry system works.

43 SEX RAPS, 45 'INCOMPETENTS'

New York City high school teacher George Addison has pocketed almost $500,000 in taxpayer-funded paychecks over the last six years -- and hasn't taught a single class. Accused of fondling a 15-year-old special-ed pupil, the veteran computer teacher has been twiddling his thumbs in a "rubber room" since 2003 ...

Addison, who has also been investigated twice for corporal punishment during his 12-year career, collects a $79,531-per-year salary for sitting in one of the city's seven "teacher reassignment centers" -- or "rubber rooms" -- while he waits for his case to wind through the backlogged disciplinary system.

Other school employees have languished even longer in the Department of Education's purgatory, which costs taxpayers $65 million annually just for staffers' salaries ... [not including of the cost of one of the world's greatest benefit-and-retirement packages that these teachers keep "earning".]

Rubber-room denizens include 43 employees charged with sex-related offenses, including 14 for relationships with students, the data shows. Another 140 were accused of employee misconduct, 117 of corporal punishment and 45 for incompetence. More than 100 were banished after being arrested.

The DOE can suspend a teacher's pay in rare circumstances, but most continue to collect checks...

During a typical day, rubber roomies show up at their assigned center by 8:15 a.m. They come and go outside as they please, and go home at around 3 p.m ... [NY Post]

As to other news of the schools and their unions this past week...

In what the Mayor and union spun as good news, the teachers union made modest pension concessions -- but took them out of the skin of the students by getting two more days added to their paid summer vacation, the days just before the opening of school when they prepared for classes.

Even the NY Times, which normally resides in the schools unions' pocket, stuck its head out far enough to run a story including criticism of the deal. Although that might be explained by the reaction of the principals' union, "The principals’ union protest set off a spat with the 228,000-member teachers’ union", which left the Times to cope with a conflict of unions. (Yes, the NYC public schools management is unionized, one more part of the problem.)Stunned principals reacted with horror Tuesday after the city agreed to have teachers return from summer break on the same day as students ....

"Do parents want their children coming into rooms where furniture is stacked up and materials packed away?" said Principal Elizabeth Phillips at Public School 321 in Brooklyn. ... Principals union President Ernest Logan said he was "dismayed" after fielding calls from angry principals "all day long."...

United Federation of Teachers President Randi Weingarten said she was not to blame ... [NYDN, more details]

But the teachers union showed it can at least teach somebody...

UFT TEACHES POL A LESSON

It's payback time for the powerful UFT. The United Federation of Teachers blocked City Councilman Simcha Felder (D-Brooklyn) from receiving an "early endorsement" from the 1.3 million-member Central Labor Council to get even with him for exposing the union's arm-twisting during a City Hall hearing on charter schools, sources said.

Felder disclosed that union reps brazenly distributed cue cards with prepared questions that legislators were supposed to ask at the April hearing. Union witnesses got the softball questions. The tough queries went to administration officials ...

"To me, it's a badge of honor," Felder said. "I think a lot of the leadership in the unions are ripping off members for their own benefit, and I don't want to have anything to do with it."... [NY Post]

Saturday, June 27, 2009

Pirate hunts of the rich and famous:

Wealthy punters pay £3,500 per day to patrol the most dangerous waters in the world hoping to be attacked by raiders. When attacked, they retaliate with grenade launchers, machine guns and rocket launchers... [Ananova]

Dumb criminal of the week.

Think things are tough for you? Get an $11-a-day job working in hell. [via Newmark's Door]

When they have to tell you it's not hyperbole, you know it is:

"The gravity of America's health care crisis is the moral equivalent of the 19th Century's bloody conflict over slavery. This is not hyperbole..." [Firedoglake, ht: Viking Pundit]Such cheap rhetorical excess literally makes my blood boil.

The day comes to us all when we are meant to die:

"Man Drowns After Being Thrown From Lawnmower" [KETV, Omaha]

In light of which, while I don't run this blog to repeat the gratuitously nasty, it can be fun.

Friday, June 26, 2009

I doubt it. I mean, in case you were thinking about buying some, be warned. Don't.

"Regular" Series EE bonds being issued today pay all of 0.7% interest.

Inflation-adjusted Series I bonds being issued today pay a nifty 0.0% through this coming October 31. This amount is comprised of an almost as nifty 0.1% real permanent interest rate to be paid over the life of the bond, plus an additional amount to account for inflation that is adjusted every six months. (In the case of deflation this later amount can reduce the total combined rate to, but not below, 0.0% -- thus the current rate).

The thing about Savings Bonds is that they usually are held as long-term investments -- people give them as gifts to newborns to provide a figurative start on college savings, grandma hides a shoebox full of them in a clost to feel secure. And so on.

They aren't marketable, and if redeemed within five years there's a penalty. But these rates are awful for long-term investments. They embody Warren Buffett's warning against being invested in long-term US bonds, writ small.

When the recession ends, and a normal economy resumes, it is hard to imagine that the 0.7% rate on today's Series EE bonds will come anywhwere close to even matching inflation, much less pay any real interest return. So they will be pure money losers, long-term. Possibly serious money losers: if inflation averages only 2.5% over the next 20 years, an EE bond bought today will lose 30% of its value by its maturity date.

(Even today, bank CDs guaranteed by the government with five year maturities, the shortest penalty-free holding period for a savings bond, pay a bit over 3% -- more than four times what EE bonds pay.)

Somewhat less bad are Series I bonds, if tradition or whatever demands that you make someone a gift of Savings Bonds. At least I bonds won't actually lose value, due to their inflation protection. Though with a 0.1% real interest rate, when they mature 20 year from now they will be worth only a real $1.02 for every $1.00 invested in them today, so your gift isn't going to make anyone rich.

The base interest rates paid on newly issued EE and I bonds is reset every six months and will change this coming November 1, but that won't really change anything of substance. Savings Bonds have simply become a bad deal compared to the alternatives.

There is speculation that the Treasury is moving towards eliminating Savings Bonds altogether, as it recently dropped the limit on annual purchases to $5,000 from $30,000. At the same time it has lowered the minimum purchase price for regular US bonds, notes and T-bills to only $100, and made it easy to purchase them online with no fees or commissions at Treasury Direct. (As recently as 1998 the minimum purchase of T-bills was $10,000).

Regular US bonds, notes and bills get better rates than Savings Bonds and are the most marketable of all securities at all times (with no penalty) so they dominate Savings Bonds two ways right there. Really, you should probably never buy a Savings Bond ever again.

About the only meaningful advantage Savings Bonds have left is that you can still buy them in paper form, stick them in an envelope and hand them to someone as a gift. But then that someone can lose or forget them. (As I can attest, regarding all the bonds I got handed for my kids.) While regular Treasury securities today are recorded in electronic format.

But you can easily make a gift of a regular T-bond, note or bill, write a note saying you did, stick that in an evelope, and everybody involved will be better off.

Savings Bonds had their run -- in an era when the Treasury issued regular bonds in denominations up to $500 million each (about $4 billion or more in today's money) to save itself the trouble and cost of processing interest coupons physically clipped and sent to it from half a million $1,000 bonds for every one $500 million bond issued.

But that era is over -- one more example of the Internet changing everything.

Wednesday, June 24, 2009

"The annual Which? Car survey is the largest survey of its kind in the U.K., and it is conducted by a publication that, like Consumer Reports, does not accept advertising and delivers the straight facts from its findings ...

"For its reliability study, Which? Car looks at models up to eight years old, thereby often reporting on years of experience with a given vehicle. Their survey tallies serious breakdowns, unscheduled repairs, and minor problems...

"Among the 38 brands featured in Which? Car, Fiat ranked 35th, followed by Renault, Land Rover, and Chrysler/Dodge ... Fiat, Chrysler, and Dodge are categorized as 'Very poor.'

"In total, Fiat, Chrysler, and Dodge provide similar reliability, and it isn’t good ..."

-- Consumer Reports.

Tuesday, June 23, 2009

What does history say about the effect on cost of government control and influence over the medical system up to now?

A look at the data is instructive. The effect of tax exemption and the enactment of Medicare and Medicaid on rising medical costs from 1946 to now is clear. According to my estimates, the two together accounted for nearly 60 percent of the total increase in cost. Tax exemption alone accounted for one-third of the increase in cost; Medicare and Medicaid, one-quarter ... [Milton Friedman]Read the whole thing.

"Poll results mean what I say they mean!"

Ezra Klein says that the latest poll results find that national health care is very popular with the public, so failing to enact it would be "resolutely, aggressively, anti-democratic" -- a denial of our responsibility in a democracy.

Paul Krugman says that the latest poll results find that the public prefers reducing the deficit over increasing government spending. But the voters "don’t know much" about policy, ”So the moral for Obama is, of course, to ignore this poll" -- anything else would be a denial of our responsibility in a democracy.

Discuss.

(H/T: John Henke)

Monday, June 22, 2009

Or, another excellent Pigouvian tax bites the dust.

The politics....

Angered by White House decisions on everything from greenhouse gases to car dealerships, congressional Democrats from rural districts are threatening to revolt against parts of President Barack Obama’s ambitious first-year agenda. “They don’t get rural America,” said Rep. Dennis Cardoza, a Democrat who represents California’s agriculture-rich Central Valley. “They form their views of the world in large cities.” ...The problem...

A rural revolt could hamper the administration’s ability to pass climate change and health care legislation ... In the House, rural Democrats threaten to marshal nearly 50 votes against the climate and energy bill backed by the administration.

... much of rural Democrats’ unhappiness with the new administration has focused on the EPA ... Obama’s EPA has moved forward quickly on a host of new regulations, including limits on greenhouse gas emissions that farm lobbyists say will raise costs on farmers... [Politico]

But that's the difficult solution, here's the easy one...Agriculture interests are scrambling to cover their rears -- or more precisely, those of their cattle -- from potential new regulation, as U.S. EPA closes in on a finding that could lead to new a regime on greenhouse gas emissions under the Clean Air Act.

Some agriculture groups and farm-state lawmakers are concerned the federal government could be forced to impose fees on livestock operations for the methane emissions that result from the flatulence and burps from their cows or pigs.

If EPA took this route, more than 90 percent of dairy, beef and hog operations could face fines, according to farm groups, with potential losses totaling $175 per dairy cow, $87.50 per head of beef cattle and $20 per hog ...

"If they do regulate greenhouse gases under the Clean Air Act, then they will have to do all sources, all emitters," said Sen. John Thune (R-S.D.), co-sponsor of the Senate cow tax bill. "That will include livestock because of the methane created and the greenhouse gas and carbon dioxide emissions in the atmosphere."...

Methane is a potent greenhouse gas, 20 times more effective at trapping heat than carbon dioxide, and a natural byproduct of the digestive process for cows and other livestock... [emphasis added] [E&E News]

~~~~

... the nation's 170 million cattle, sheep and pigs produces about one-quarter of the methane released in the U.S. each year, according to the Environmental Protection Agency. That makes the hoofed critters the largest source of the heat-trapping gas.... [a] contributor to global warming bigger than coal mines, landfills and sewage treatment plants ..

Research has shown that changing cattle diet and boosting efficiency — such as producing the same amount of milk and beef from a smaller herd — can result in less gas, according Frank M. Mitloehner, an associate professor at the University of California at Davis, who has studied livestock gas for 15 years."I don't think livestock should be ignored. Every industry has to play their role," Mitloehner said. [ AP ]

House appropriators approved a $10.6 billion spending bill for U.S. EPA last night, tucking in several amendments aimed at insulating agricultural interests from the reach of federal climate regulations ... [including] provisions to block EPA regulations requiring factory farms to report their greenhouse gas emissions and exempt livestock operations from possible carbon regulations.So as city people get hit with global warming taxes farmers get off free -- and cow gas remains a threat to burn the world ...

... agriculture groups and farm-state lawmakers are concerned that if EPA moves to regulate greenhouse gases under the Clean Air Act, EPA could impose fees on livestock operations for the methane emissions that result from the flatulence and burps from their cows or pigs..

... the amendment would prohibit EPA from requiring Clean Air Act permits for carbon dioxide, methane and other greenhouse gases emitted by livestock... [ NY Times ]

Sunday, June 21, 2009

Fathers of the day

George Stephanopoulos, just named Father of the Year by the National Father's Day Committee, said he was certain the title would be revoked due to a recent radio broadcast from his home in which one of his daughters could be heard screaming at him, "I hate you!" ... [P.6]From a poll, top responses....

Oh, the joy of being a dad.Creepiest celebrity dad? ... Michael Jackson, 52%.

Worst famous father? ... Michael Lohan, 36%.

How much do you plan to spend on your dad's Father's Day gift? ... Nothing, 36%.

Fathers, what is the best Father's Day gift you could receive? ... Time alone, 43%.

Friday, June 19, 2009

The strange case of the dog that isn't barking over the $134 billion of bearer bonds.

Revised: I've added a couple more possibilities to cover all the bases, and a few more thoughts, after a fun discussion with some associates.

~~

Three days ago we told the story of the detention in Italy of two Japanese nationals crossing the border into Switzerland who were found by border authorities to be carrying $134 billion in purported US bearer bonds in the false bottom of a suitcase.

Three days ago we told the story of the detention in Italy of two Japanese nationals crossing the border into Switzerland who were found by border authorities to be carrying $134 billion in purported US bearer bonds in the false bottom of a suitcase.Since then a very strange thing has happened: Nothing.

This story has gotten a lot of play in Europe, but US media coverage has been virtually zilch (as of when I checked Google News a couple hours ago). Even at Bloomberg, the only US news agency to file original reports in the subject, however brief, the longest piece has been an opinion column wondering how strange it is that nobody has been reporting the story.

And it is indeed strange because either...

A) The bonds are counterfeit, and this is one of the largest counterfeiting frauds in history; or

B) The bonds are real, and represent a potential earthquake-blow to the world financial system in the midst of the ongoing financial crisis, as some major government has tried to get out of US bonds and dollars in a big way, on the sly.

Isn't either of these a real story?

Moreover, on its surface this appears a case worthy of Sherlock himself, because each of the two major obvious possibilities seems, well, incredible to the point of being impossible.

[] Scamming someone into buying $134 billion of fake bearer bonds would be considerably more difficult than scamming them into buying a fake Mona Lisa. If Mona wasn't missing from the Louvre, any buyer would immediately know any copy being offered is a fake. If Mona was reported missing from the Louvre, well, it's possible a fanatic art lover might pay to buy a copy passed off as the real thing to hang in his den and admire until he dies, I guess.

But people buy US bonds for the dividends they pay and to cash them in. These bonds were issued in denominations of $500 million each. Nobody is paying for those without calling up the Fed to verify that they are real. Which is easy -- call, give the Fed the serial numbers and other descriptive information, and it replies, "No, fakes" or "Yes, real, and owned by the Chinese government to whom we are paying interest", and if you aren't buying from the central bank of China you know the bonds are either fake or hot, and you aren't going to get your money back from them. End of scam.

Moreover, who could buy $134 billion of US bonds? -- $134 billion is more than the GDP of New Zealand. Only the Chinese, Japanese and Russian governments own that much. Major governments like them are the only buyers, they all have hotlines to the Fed, and they aren't going to be scammed.

A counterfeiter would be better off producing mere millions of dollars of fake currency or of, say, $10,000 bonds that could be peddled to many buyers. How a $134 billion scam could even be conceived is ... hard to conceive.

So, Sherlock might say, eliminating that as impossible we have these possibilities ...

[] The bonds are real and were being moved by the Japanese (or Chinese) government to get out of the bubble in US bonds before it bursts, via an "under the table" trade in Switzerland for something else of value -- instead of by making market sales that would themselves bust the bond bubble in ways that could rebound against the seller (grievously!). That's an idea that in fact may make sense on its face.

But why would the Japanese government move $134 billion into Switzerland by taking the crazy risk of having a couple guys try smuggling it in a suitcase on a train reportedly full of itinerant workers, through a border crossing known for smuggling, and so subject to scrutiny by customs authorities? Wouldn't it instead use the near absolutely safe option of sending the bonds by diplomatic pouch?

Which makes us look at parties who can't use a diplomatic pouch. Maybe...

[] The bonds are fake and were sent by a "rogue" nation. It would take a government to work a deal on the order of $134 billion. And maybe, say, the North Koreans would try to pull something like this off with a third party. Yeah, they'd have to be nuts, and ignorant of how western finance works -- but they are. And the North Koreans are well known for mass counterfeiting of dollars, either to pay their own bills or as an act of economic warfare (or both) -- perhaps they decided to "go nuclear" with the option? Or maybe...

[] The bonds are real and were sent by a "non-official" person from a foreign nation. The few news stories published on all this typically say that the US stopped issuing bearer bonds in 1982. But, as I noted in my prior post, the law that ended the issuance of bearer bonds in the US contains exceptions that enables the Treasury to still issue them to foreigners.

Now imagine, hypothetically, that the Chinese government, for reasons of its own, asked that, in exchange for its continued support in financing the US deficit, the Treasury issue some of the bonds it was buying in "bearer" form, and that the Treasury did. The Chinese government still has roots in communism, is trying to make the jump from third-world to first-world in one generation, and is rife with factionalism. Suppose next that the bearer bonds wound up in the hands of an individual government functionary, and he decided to keep them under his personal control to secure his position and "influence" over the government, not to mention a well-funded retirement. Might those bonds then find themselves on their way to an anonymous safe deposit box in Switzerland?

This idea eliminates the awkward requirement of a buyer for the bonds, and offers entertaining James Bond-type story possibilities. But why would the government of nation like China ever open itself to such a risk by demanding bearer bonds, rather than registered bonds, in the first place?

Well then possibly the bonds are fake and not from a government ...

[] The bonds are fake and part of a small-money "Nigeria"-type scam. In this the scammer claims to hold some huge asset, but for some strange reason needs your help to cash it in, in the form of an advance payment of money from you, in exchange for which he promises you a share of the asset after he cashes it in. (Nigeria scams require seemingly unbelievable stupidity on the part of their victims -- but experience shows human stupidity is something one can always safely believe in.)

I guessed before that "Probably this was all some lunatic scam gone bad, a 'Nigerian' scam of insane proportions" -- primarily because it gets the dollar amount involved down to plausible levels. Making it even more likely, it turns out that this scam has been pulled with bearer bonds before. (ht: Newmark's Door)

But the idea of a Nigeria-scam still leaves plenty of questions: This scam has to be pulled on rubes, real dummies. You need a big market of people in which to find them -- the big old USA, as in the linked example, is fine! But if you were going to pull this scam using fake bearer bonds, why would you smuggle them into Switzerland, which has probably the smallest and most financially astute population outside of Liechtenstein?

It doesn't seem like anyone would take these bonds into little Switzerland unless there was someone there already committed to wanting them. Who? Moreover, with a Nigeria scam the victim wouldn't be buying the bonds, acquiring them, but would be paying money to help the scammer dispose of them. So why would the bonds be going into the country at all, instead of the victim's money going out?

And why all the secrecy after a routine Nigeria scam was busted? Shouldn't they be publicizing it as a public service, a lesson on consumer safety?

I think the five general scenarios above cover all the logical possibilities (real/fake bonds, govt/non-govt actors, etc.).

But there are two more peculiarities about this case that are odd in any scenario...

[] Nobody's been arrested(!) Multiple reports say this -- and even that the two men carrying the bonds have been released.

Yesterday the mystery deepened as an Italian blog quoted Colonel Rodolfo Mecarelli of the Como provincial finance police as saying the two men had been released. The colonel and police headquarters in Rome both declined to respond to questions from the Financial Times.These two guys either were part of the one of the biggest counterfeiting scams in history or owe 40% of $134 billion -- that's $53.6 billion -- as the penalty under Italian law for smuggling undeclared real securities over the border ... and they've been released? (Does this suggest they have the protection of a legitimate government??)

Even if this was "merely" a Nigeria-type scam involving $134 billion of forged securities being smuggled over the border, would you expect the perps to be released and allowed to walk away?

[] The news blackout. After the initial reports from Italy, there's been virtually nothing of substance reported of any kind. Why? If the bonds are fake and this was a routine scam of some sort, why not say so and give the details? Why were the smugglers released? Who where the smugglers? The most simple fact of whether or not they were really even Japanese hasn't been confirmed.

The initial multiple reports from Italy said that the bonds if counterfeit are excellent counterfeits (although how many $500 million US bonds do local Italian police see? so how would they know?) and that US authorities have been asked to examine them and are expected to do so next week.

But today a brief statement from the Fed declared the bonds to be fake even without examining them. "Based on the photos we've seen on the Web, they're not even close to looking like a Treasury security." [WSJ] They are judging by photos on the Web? Like this?

All of this has me putting on my Holmesian deerstalker cap, and for the first time in my life seriously considering ... maybe ... conspiracy theory.

If the bonds were real and you were the US government, what would you do? I'd think...

1) Declare definitively that the bonds are "fake" (no need to even look at them) to protect the world financial order in general and the value of the US dollar and US debt in particular, then...

2) Suppress all media investigation into the genuineness of the bonds, for obvious reasons, and then, just maybe...

3) Burn the bonds! Subtract that $134 billion from the national debt. Why not? The bonds are fake, right? Is the government of Japan (or China) belatedly going to say: "No, no, the bonds are real! Hey, give them back to us! We were just trying to smuggle them onto the world's financial black markets ..."? I doubt it. Why not teach 'em a lesson and save the taxpayers some real money at the same time?

Well, I'm not quite a conspiracy theorist yet. If I was forced to wager, I'd still put my money on "Nigeria scam" as least implausible.

I don't know what the truth is -- but shouldn't any of these possibilities be a real story for the press?

Whatever went down, something happened on an historic scale: attempted fraud, smuggling, forgery, act of economic warfare, James Bond-like intrigue, Nigeria scam, something. The news blackout itself would seem to be a story.

Yet not one hound in the entire pack of the press is barking. Which seems very strange, considering all the endless inanities that the entire pack goes yap! yap! yap! yap! yapping about all the time.

It's a mystery to me.

Thursday, June 18, 2009

Freedom in the 50 States: An Index of Personal and Economic FreedomMy state ranks dead last. Some commentary on the fact.

-- from the Mercatus Center, George Mason University

A star to generations

A recent e-mail exchange:

"My spellchecker keeps changing Krugman to Kurgan. What's a Kurgan?"

"The Kurgan? From the Highlander films?"

Aye! Of course! Clancy Brown, best known to my generation as Kurgan, the most vile, would-be immortal villain, murderer of Sean Connery's Juan Sánchez Villa-Lobos Ramírez, mortal foe of Christopher Lambert's Highlander.

video: "Most badass scene ever"

Best known to my kids as Mr. Krabs, eccentric money-obsessed proprietor of the ocean floor's favorite burger stand!

video: It's never closing time at the Krusty Krab!

Now there's an actor with range. (Gene Hackman, eat your heart out.)

Wednesday, June 17, 2009

A message from GM back when it was an innovator that knew how to sell cars [at 6:15]...

"on what other car will you find the combination of all these luxury features, such as this year's front vent pane control crank, ordinarily found in only the highest priced cars"...today how many people are old enough to even remember seeing a front vent pane window on a car?

How to read the Wall Street Journal online for free. You can't have your stuff indexed by Google and keep it locked behind a pay wall too, Rupert. (via Newmark's Door)

Dedicated professionalism quote of the day:

"I was still at the stage in my career when I was trying to work really hard and do a good job."

-- Sigourney Weaver on filming Ghostbusters.

The next financial crisis: "A major credit rating agency yesterday released a report reinforcing a negative outlook on the financial stability of the toll road industry" predicting "massive toll increases coming".

OK, now Krugman has to stop complaining about people mispronouncing his name. [.pdf]

Milton Friedman is gone, but his co-author Anna Schwartz is still with us.

Discrimination against white customers in the prices charged at the Fulton Fish Market? (via Carpe Diem)

For those who like to imagine they are racing down the slopes while sitting on the pot, from Japan of course.

An Internet classic: Blond with gasoline can.

Tuesday, June 16, 2009

That's a question being asked in several countries today...

Japan is investigating reports two of its citizens were detained in Italy after allegedly attempting to take $134 billion worth of U.S. bonds over the border into Switzerland...A story that raises interesting questions!The Asahi newspaper reported today Italian police found bond certificates concealed in the bottom of luggage the two individuals were carrying on a train that stopped in Chiasso, near the Swiss border, on June 3.

The undeclared bonds included 249 certificates worth $500 million each, the Asahi said, citing Italian authorities. The case was reported earlier in Italian newspapers Il Giornale and La Repubblica and by the Ansa news agency... [Bloomberg]

Multiple reports (do you read Italian?) describe these as "bearer bonds", as they pretty much would have to be. Regular US bonds have registered owners, so they can't be traded surreptitiously, and today don't even exist on paper but only as electronic bookkeeping entries, so they can't be packed in the false bottom of anything.

Bearer bonds date back to the 1800s, as a type of bond for which possession is 100% of the law. The person who possesses a bearer bond owns it, and title to it passes upon delivery to the next person. There is no registered bond owner of record. Bearer bonds are the bond world's equivalent of "cash", with the advantage that they can be issued in massive denominations -- US government bearer bonds have been issued in amounts up to $500 million. (Not exactly Montgomery Burns' trillion dollar bill, but the real world's closest thing to it.)

As such in the 20th Century bearer bonds found great use in tax evasion and money laundering. In the U.S. that largely ended in 1982 when Congress enacted the Tax Equity and Fiscal Responsibility Act, which in addition to repealing a good portion of Ronald Reagan's famous tax cuts of the previous year, also stopped federal issuance of bearer bonds and taxed new issues of corporate, state and municipal bearer bonds out of existence.

But previously issued bearer bonds are still out there, and "traditionalist" bond investors still head to their safe deposit boxes every six months to clip the coupons off them to collect their interest. The US issued bearer bonds with 30-year and 50-year maturities, so some are still around.

But $134 billion is a heck of a lot of bearer bonds to be found in one false bottom of a suitcase! The only nations that own more US debt than that are Japan, China and Russia, so if those bonds are real the guy who was carrying that suitcase is/was the United States' fourth largest creditor.

It's hard to believe such a load of bonds can be real -- but it's also hard to imagine any kind of scam involving so many fake bonds.

While the owners of US bearer bonds are unregistered, the bonds themselves are easy to check out by calling the US Treasury with their serial numbers and asking about them. Is anybody buying $134 billion of bonds not going to do that? Even if getting a big discount on the purchase price? I mean, this is not unloading a suitcase of freshly printed $20s. It seems unimaginable that anyone would take them without verifying them. (Yes, "there's a sucker born every minute", but that would be one special kind of $134 billion sucker!)

On the other hand, could the bonds possibly be real? In that case there's no problem verifing them, they have the value of real money. But where could that much money possibly have come from?

There was a loophole in that law of 1982, TEFRA's anti-bearer bond provisions were aimed at bonds issued domestically -- there were exceptions that enabled bearer bonds to still be issued to foreigners.

Has the Treasury quitely been issuing bearer bonds to the Japanese, in response to some "special request", to fund the US deficit? And if the Japanese Ministry of Finance one day found $134 billion of bonds missing, would it let anybody know? "Oooops! Hey, has anybody out there seen...?"

I have no idea. What would you be doing with $134 billion of bearer bonds (real or fake) in a suitcase?

Monday, June 15, 2009

Last week we saw the story of New York Metropolitan Transit Authority train yard workers who pull down overtime pay on the order of $200,000 a year on base salaries in the range of $60,000 to $70,000.

Hey, that's a lot of overtime pay! A logical question that popped to mind (though not pursued here at the time) was: how many overtime hours did those guys have to put in to earn that much? Well, let's guesstimate...

Earning time-and-a half totaling $200,000 on a salary of $60,000, assuming a base work week of 40 hours, would require another 89 hours of work a week .... plus the original 40 hours ... for a total of 129 hours of work per week ... every week of the year!

And 129 hours a week divided by a five-day work week is 25.8 hours a day. So let's assume a seven-day work week. That's still 18.4 hours a day, seven days week, every week of the year.

Geeze, to get paid for that many hours, it looks like they'd have to get paid for sleeping.

And guess what ... they were!

So after getting paid for say 24 hours of overtime on a "job" that didn't have to be done to begin with, one gets to go home and get paid double-time for another eight hours of watching TV or sleeping it all off....They get cash for catching Zzzz's!

An arcane union rule allowed 34 Long Island Rail Road grease monkeys at a Queens maintenance shop to earn a total of $2.5 million in overtime last year, and some of that staggering sum was paid just for heading home and going to bed, The Post has learned ...

Under the rule, the railroad is required to fill vacant slots on all work shifts -- regardless of whether the manpower is needed -- allowing senior repairmen to pick up enormous amounts of extra hours.

If a repairman is out sick or goes on vacation, for example, the rule requires the shift's empty slot to be filled by another mechanic, even if he's not needed or on OT.

There were hundreds of instances last year when mechanics worked 24 to 32 hours straight, racking up time-and-a-half and double-time pay. The system then dictates that these OT kings be sent home to collect an additional eight hours of pay for no work.

Many accrue 40 consecutive hours of pay in a single stretch, ringing up a full week's wages in less than a day and half.

And the gravy train doesn't stop there. Another mechanic can then pick up the vacant slot left by the sent-home worker and receive time-and-a-half pay.... and while one is getting paid double-time for sleeping at home, someone else gets to step in and collect time-and-a-half for doing the very same job. Which leaves the MTA paying, what, triple-and-a-half time, for a job that didn't have to be done at all.

Plus there's the salary of the guy out on vacation that the other two are filling in for. Quadruple-and-a-half time?

'Nuff said. Because as a New Yorker who's paying that fare hike and the new taxes for that bailout, I can't bear to say any more.As The Post reported last week, the biggest earner was Ronald Dunne, who took home $283,373 -- nearly $220,000 in OT...

The huge paydays come at a time when the MTA ... approved a 10 percent across-the-board fare hike and got a $2.3 billion taxpayer bailout to plug a gaping hole in its 2010 budget.

Snark versus snark, Krugman Monday edition.

A Republican politician, House Minority Leader John Boehner, takes a partisan political shot at the Obama stimulus, saying that a good four months after it was enacted jobs are still being lost. It's a literally true yet dubious critique, as careful partisan political shots are wont to be.

The literally true part is that, yes, jobs are still being lost. The dubious part is that even true believers in the stimulus don't expect it to do much before much of the the stimulus money is spent, and that whatever the employment numbers may be they might well be worse without the stimulus -- nobody knows for sure, and nobody will know until the econometric studies of it come in five years from now, and people will argue about it then.

Krugman could've replied honestly along these lines. But being who he his, he shoots back a return snark that lowers the bar to below a deceivin' politician's level by having zero relevant truth at all. To wit...

~~~~

Stimulus history lesson

Just sayin’:

~~~~

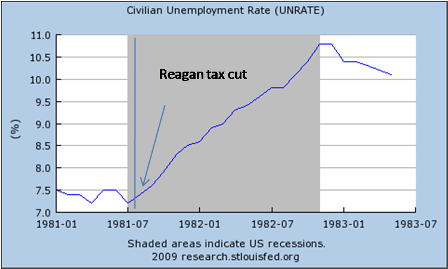

Huh? What is the relevance of this? That the Reagan tax cuts supposedly caused the '82 Recession? Didn't stop that unemployment? What's this supposed to have to do with the Obama spending increase stimulus?

Especially since the '82 recession was entirely caused -- as Krugman well knows -- by the Fed pushing up interest rates to all-time, still-record highs to break the double-digit inflation inherited from Jimmy Carter .

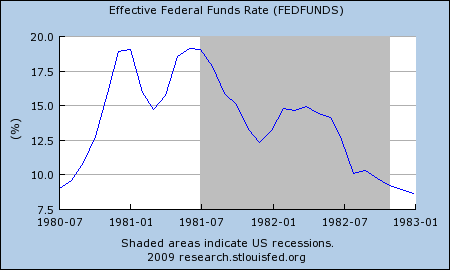

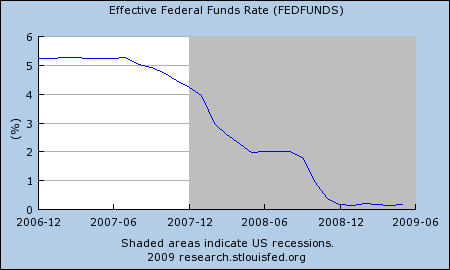

Well, here are two more charts. We might call them, "Stimulus history lesson II".

In the first we see the Fed pushing interest rates up to the record highs (19%!) and, one year later, exactly with the time lag the textbooks predict, the fall in the economy and increase in unemployment caused by the huge interest rate hike, which dominated the effect of the tax cuts, as the Fed intended them to do.

In the second we see that in the same year-long period before the current recession, interest rates were flat (just over 5%), never rose, and that in fact six moths before the recession started they began falling to an all-time low (effectively 0%) -- and that even reinforced by this historic lowering of rates (plus massive "quantitative easing" to boot) the Obama stimulus has left the economy still falling and unemployment rising.

I mean, I don't want to imply any false conclusions on the basis of any of this.

I'm just sayin'.

Though one conclusion we might reach from all this is that Krugman is even more deceptive than your typical known lyin' politician.

Sunday, June 14, 2009

National debt road trip video. Which presidents put the most miles on the odometer?

The problem with bailouts, in pictures. [via AdamSmith.org]

Your stimulus money at work.

How much 2009 college graduates will lose from their future earnings to the taxes needed to finance Obama's deficit increases.

One nutcase makes all racists look bad:

"The responsible white separatist community condemns this. It makes us look bad." -- John de Nugent, acquaintance of James W. von Brunn, the Holocaust Memorial Museum shooter. [Wapo]

William Easterly on the United Nations on human rights:

So here’s the scorecard on UN human rights. On something like “the right to water,” where it is impossible to identify who is violating such “rights,” the UN talks big. On human rights violations like killings and torture, where the UN knows precisely who is the violator, the UN sometimes shows up on the violator's side.

Did GM's bosses not know its cars were crap because they were tested at a Potemkin proving grounds?

And on the happier side of things...

German schoolboy survives getting hit by meteorite. "At first I just saw a large ball of light, and then I suddenly felt a pain in my hand..."

Japanese scientists create "glow in the dark" fluorescent monkeys.

New plasma blowtorch will get your teeth really clean. ("Plasma is the future" says the university researchers' news release. Remember when the electric toothbrush was the big Christmas gift?)

The meat dress, home-stitched from salami and bacon. "I badly wanted to go to a vegan restaurant in it." (She's cute, sews, and has a sense of humor too. Why did I never have a girlfriend like this?)

Markets in one less thing:

The 22-year-old California virgin who auctioned off her virtue online for $3.8 million has yet to meet her winning bidder in the flesh -- because his wife won't let him.

Natalie Dylan ... got a phone call from the rogue Romeo, a 38-year-old Australian real-estate businessman, who said he had to back out. "I told him to go back into marriage therapy," sniped Dylan.

The Aussie cad then sheepishly asked for his $250,000 deposit back.Dylan said no hard feelings; it would be returned.

Friday, June 12, 2009

So far it's only a suggestion...

The head of China's second-largest bank has said the United States government should start issuing bonds in yuan, rather than dollars ...Maybe the Chinese have been listening to Warren Buffett, who at the end of February in his annual letter [.pdf] to Berkshire Hathaway shareholders warned against today's "bubble" in US Treasury bonds...

It was the first time the head of a major Chinese bank has called for the wider use of the yuan, although a chorus of senior government officials have already voiced their concerns about the stability of the dollar and have said the yuan should be used more widely ...

Guo Shuqing, the chairman of state-controlled China Construction Bank (CCB) ... is a former head of China's foreign-exchange administration, which manages the country's $1.9 trillion foreign exchange reserves ...

Two months ago, before the G20 meeting in London, Zhou Xiaochuan, the head of the People's Bank of China, the central bank, published a personal paper proposing to replace the dollar as the international reserve currency. His call came after Wen Jiabao, the Chinese premier, asked the US to guarantee the safety of China's huge pile of US debt ... [Telegraph]

When the financial history of this decade is written, it will surely speak of the Internet bubble of the late 1990s and the housing bubble of the early 2000s. But the U.S. Treasury bond bubble of late 2008 may be regarded as almost equally extraordinary.If you were the Chinese government currently holding some $800 billion of US bonds, how would that make you feel?

Clinging to ... long-term government bonds at present yields is almost certainly a terrible policy if continued for long.

Especially since China, for all the talk of it becoming an economic power, is still a poor country, with GDP per capita (at purchasing power parity) of only about $6,000, compared to about $47,000 for the US. So $800 billion to them is by that measure almost eight times as much as it is to us -- call it $6 trillion, in our terms. That's a lot have invested in an "historic bubble".

As long as the Chinese keep investing their money in our debt denominated in our dollars, they can lose three ways...

[] As interest rates on US debt rise from their recent historic lows, the price of US debt obligations will fall, since bond prices move inversely to interest rates.

For instance, 30-year US bonds earlier this year were paying less than 3%. If the Chinese bought any of those, and the rate on 30-year bonds returns to a much more typical 6% in the near future, the market value of those bonds will drop per $1,000 to under $600, a cool 40% decline.

[] The exchange rate value of the dollar can be expected to drop from its surge level of the financial crisis that saw it rise by almost 20% in recent months, as foreigners rushed into the dollar in the "flight to safety" to buy US debt, sharply reversing a long slide in the dollar's value that began in 2001. But now the dollar has begun going down again.

If it only goes back to where it was, the loss of the dollar value of those 3% bonds will be compounded by the corresponding loss in the value of the dollars they are valued in. Ouch. And the long-term decline in the value of the dollar may resume from there, as the US continues to run historic fiscal and trade deficits.

[] The value of the dollar itself may drop if inflation rises in coming years, as has been known to happen to the currencies of countries that run massive deficits indefinitely, as the US government now is planning to do.

Put all the above together, and you can see how the Chinese would sleep better at night if they were loaning all that money to us through bonds denominated in their currency rather than our currency.

Of course, right now they are offering that idea only as a suggestion...

Why not to stuff your money in your mattress.

JERUSALEM -- An Israeli woman mistakenly threw out a mattress that she said had almost $1 million inside, setting off a frantic search through tons of garbage at a number of landfills yesterday.

The woman told The Associated Press that she bought her elderly mother a new mattress as a surprise present on Monday -- and threw out the old one.

The next day, she said, she remembered that she had hidden her life savings inside the old mattress. "I woke up in the morning screaming, when it hit me what happened," said the Tel Aviv woman, who asked not to be identified.

She went to look for the mattress, but it had already been hauled away by garbage collectors, she said. Searches at three different landfill sites turned up nothing.

She said the money was in US dollars and Israeli shekels. She refused to say how she acquired such a large sum. "It was all my money in the world," she said...

The Israeli daily Yediot Ahronot published a picture of the woman searching through garbage at a dump in southern Israel. The picture shows the woman, dressed in a white top and black pants with her back to the camera, picking through a huge pile of trash that fills the frame about 10 feet in all directions.

Yitzhak Borba, the dump manager, told Army Radio that his staff was helping the woman, saying she appeared "totally desperate." He said the mattress was hard to find among the 2,500 tons of garbage that arrives at the site every day.

He said he increased security at the site to keep would-be treasure hunters away.

The woman said the money had been stashed in a mattress because she had had "traumatic experiences with banks" in the past. She would not elaborate. [NY Post]

Wednesday, June 10, 2009

If it doesn't rain, today New York's state senators will be meeting in the park across the street from State Senate Chamber in Albany. The Democrats who ran the senate until yesterday and still possess the keys to the iron gates at the Chamber door have locked them, to keep the newly ascendant Republicans outside.

Thus the Empire State is governed.

Megan McArdle, commenting on the "coup" pulled by the Republicans yesterday in getting two senate Democrats to switch to their side and turn the balance of power, wrote that where she is the story "... is being reported nearly exclusively as a gay marriage thing. Yes, I understand that this is a blow to gay marriage..." So I'll take it that outside of New York that political spin being applied.

But no, it is not a "gay marriage thing", not at all. Governor Patterson wishes it were a gay marriage thing! More of that in a moment...

The gist of what happened is: The Albany Democrats in the state senate have been out of power for 43 years and, shall we say, lack management experience when it comes to actually doing things, as opposed to posturing for various audiences. In last year's election they won control of the state senate by just one vote -- importantly, less than one solid vote, because immediately after the election no fewer than four dissident Democrats threatened to switch to the Republicans, which caused them all to be bought off, for the moment, with many promises.

Now you might think that a new Democratic leadership handicapped by such a precarious hold on power might act cautiously to shore it up, adopting judicious policies, perhaps even trying to lure over some Republicans from the other side to join them and secure their majority. But you would be wrong.

Instead, with absolutely no experience at managing power, the Democratic leaders went on a rampage as if they had the FDR majority of 1933. They broke their promises to their main backers in general and potential defectors in particular. On the strength of their shaky one-vote majority they fired hundreds of Republican staffers and employees ... slashed millions of dollars out of the Republican senate operating budget ... moved Republicans to former-closet offices in the basement and under the stairwells ... distributed the senate's pork, er, "member items" at a ratio of $78 million for Democrats to $8 million for Republicans ... etc. & so on.

One might say they demonstrated the keen perception, nuanced judgment and subtle tact of Eliot Spitzer.

By doing so they unified the Republicans as their bitter enemies (when in their moment of weakness wavering Republicans might have been co-opted) and antagonized the entire Albany "professional political establishment" which has considerable influence of its own (think "Yes, Minister", on this side of the water).

A critical individual player in all this was Tom Golisano, an upstate entrepreneurial billionaire and "good government" activist. Despite being very much the businessman and a low-tax, low-regulation guy, he gave millions of dollars to the Democrats in the last election to help them win the senate. He'd given up in disgust on the Republicans and their 43-year record, concluding the Democrats couldn't possibly be worse. He soon found out how wrong he was about that.

After taking his money the Democrats not only broke all the promises they made to him about enacting "good government" reforms, they also decided to close an $18 billion budget deficit by increasing spending by 8%, financed by 52 new taxes, including a new higher top tax bracket rate on him. (This would cause him to announce that he his moving his residence out of the state to save $13,000 per day in taxes ... but that would be later.)

Moreover, they slighted him personally. When Golisano met with the new Democratic Senate leader Malcolm Smith to discuss these events -- particularly to propose ways to close the state budget gap without raising taxes -- Smith snubbed him by playing with this Blackberry throughout...

"Of course I was upset ... When I travel 250 miles to make a case how to save the state a lot of money, and the guy comes in and starts playing with his Blackberry, I was miffed."So Golisano flipped sides and told the Democrats' "fickle four" that if they went over to the Republicans he'd back their re-election campaigns with his money no matter what the Democrats did to them. And then they all spent about the last two months planning yesterday's switch.

During which time the Democratic senate leaders were so politically astute that they didn't have a clue that any of this was going on. Not until a vote on the distribution of pork, er, "member items", started shockingly to go against them yesterday. At which point they turned out the lights in the chamber and stopped the TV broadcast of events, much like a third-world junta tries to stop news of an uprising against it from reaching the public. With the same result.

Of course the immediate aftermath has been a deluge of personal slurs and charges of political treason, extortion, bribery, corruption, and other assorted wrongdoing -- and they are all true! Everybody is accusing everybody else of being "the bad guy" -- and they are all right! But as Golisano put it...

"Don't talk to me about ethical backgrounds in Albany. We have a governor who stood on a podium on national television and said he had extramarital affairs and used cocaine."No, this is not a story about gay marriage. It is a story about hardball politics ... and of stunning political incompetence by the Democratic leadership in the state senate which for 43 years had been selected and bred to do nothing but posture -- and which when given a modicum of actual political power went bat s**t crazy with it and self-destructed.

Governor Patterson wishes this was a story about gay marriage, since it appears to be the one and only issue working for him with the voters here. And since, as a result of the senate power switch, he looks about to get hoisted good-and-high on his own political petard.

Patterson, the "accidental governor" who took over when Spitzer self-destructed, reportedly has the lowest poll numbers of any governor in the nation. To try to boost them he has been posing as a fiscal moderate against the tax-and-spend Democrats in the legislature, by proposing "fiscal reforms" such as a state spending cap limit, property tax limitations, and so forth.

In doing so he has been engaging in one of the oldest of political shams -- supporting what he knew there was no chance the legislature would ever pass. He would enjoy getting all the high taxes to spend while posing as being against them.

But now -- horror of horrors! -- he actually faces getting what he's asked for! The Republican senate says it will pass his proposals. And that will put him in the position of either having to join the Republicans in backing his proposals against his own Democratic party, and probably losing right there whatever minimal chance he may still have of getting its nomination for another term ... or of joining the Democrats in fighting his own proposals, showing all the voters he never meant them and displaying what a lyin' politician he's been all along.

The governor is the big loser in all this (apart from the senate Democrats themselves -- maybe even bigger than them, since they'll almost all at least keep their jobs thanks to gerrymandering, while the governor figures to end up unemployed).

The big winner (apart from the senate Republicans) is Mayor Bloomberg. It's not at all clear at this point whether he played a role in these events or not. But Bloomberg has a lot more influence with senate Republicans than Democrats, and the Republicans are a lot more sympathetic to some of his top priorities, such as keeping mayoral control of the school system. Bloomberg has kept a very low profile in discussing these events, and is not crying over them. We shall see.

Are there some larger lessons for all of us, even non-New Yorkers, that may be drawn from these events? I suggest there are...

[] Republicans, even when facing the most trying of times, always have one thing going for them: Democrats.

[] In two-party politics, big power shifts almost always come not from the challenger party successfully challenging but from the incumbents screwing up. (Give Obama and the national Democrats some more time.)

[] Anybody who wants this class of human being ... politicians... to design and manage national health care or any other similarly grand public ambition is ... well ... not familiar with our real world.

Do not think of nationalized health care and such great public schemes as being designed and run by "the government", wisely and on our behalf. Think of them as being designed and run by politicians, by these guys.

These very guys have already brought us government-run health care, Medicaid, that is 40% fraud and "legal graft", and public transit that pays repair yard workers $280,000 a year at the taxpayers' cost. How much more do we want them to do for us?

Watching the politicians of the New York State government in Albany in action will make a libertarian out of anybody!

If Gus Hall were still alive today, it would make a libertarian out of him.

Do you really think politicians in Washington DC are so different?

Monday, June 08, 2009

While New York's Metropolitan Transit Authority needed a $2.3 billion bailout this year including, in addition to fare increases, a new regional payroll tax, a new (uncollectible) tax on taxi trips, and more....

grease monkeys at a [MTA] maintenance facility in Queens ratcheted up their incomes by more than three times their base salaries through enormous amounts of overtime and other perks in 2008, according to payroll records obtained by The Post.Which is critical. The MTA pays full pensions at age 55, with the size of the pension determined by the last few years of compensation (not salary).

The biggest payday went to Ronald Dunne, a car repairman who pulled down a staggering $283,373 in total compensation ... Dunne's base salary was $62,976 but, incredibly, he hauled in an additional $220,397, mostly from overtime ...

Dunne works at a diesel train yard in Richmond Hill, Queens, which has been an overtime gold mine for employees.

Another LIRR car repairman, Michael Visceglia, took home $274,765 in 2008 ... The 28-year employee earned $211,789 -- most of it overtime -- on top of his $62,976 salary.

Another Richmond Hill yard employee, road car inspector and former repairman Michael Shurman, made $278,746 in 2008, and retired in November of that year. Retirement has been just has lucrative ... he now gets a monthly pension check of $10,122....

Shurman's salary was $71,595. His pension is $121,464.

Three other yard mechanics were overtime kings of Queens: Donald Brooks, Michael Gilmore and Brian Delgiorno, who took home a cumulative $664,265 in 2008...Ya' think?

Delgiorno, who retired in September after 31 years, made $62,976 in salary plus $106,385 in overtime. He also cashed in $38,410 in unused vacation and sick days. He now collects $9,768 a month from his pension ... [$117,216 annually, versus salary of $62,976]

...mechanics weren't the only employees who got windfalls from the LIRR. Conductor Shelton Bethea made $241,203 before his retirement in November 2008. He took home in $78,030 in overtime and cashed in $89,980 in sick and vacation days. His pension now pays him $7,408 a month. [$88,896 versus $73,193 salary] ...

"When you have someone earning close to five times their base salary in overtime, it raises serious questions about management," said Gene Russianoff of the Straphangers Campaign...

"Whenever you see something like that, it does raise a red flag," said Bill Henderson, executive director of the Permanent Citizens Advisory Committee to the MTA.

Yet amid all the political trauma -- and threats of "doomsday" service cuts if the fare increases and all the new taxes weren't enacted -- the politicians spoke nary a word about "controlling compensation and pension costs".

Go figure.

~~~

Update: Maybe that was because they don't want their own pensions questioned.

Pension costs for elected politicians, mayoral appointees and their staffers are forecast to shoot up 26 percent over the next five years ...

Even the man who helped put the fearsome financial forecasts together, Charles Brady, assistant director of the Office of Management and Budget, retired last year with a staggering $142,074 pension...

Sunday, June 07, 2009

"Assume a can opener". The take on the Obama Administration's plan for containing rising health care costs, as part of its national health care proposal, as per Andrew Biggs.

These costs savings are what [budget director] Orszag in his Social Security days called a "magic asterisk," money that materializes out of nowhere.

"Deficits matter", says Andrew Samwick.

the Obama administration has announced a target of reducing these bloated deficits in half in five years. That means that we are running these deficits even as the economy is projected to be growing again. That's just as pathetic, but on a much larger scale, than the budget target we had under the Bush administration.That's my emphasis added in the quote, but it is a much larger scale. The Obama deficits incurred in two terms are on course to be as large as the Bush and Reagan deficits incurred over four terms, combined. Speaking of which...

A first small sign of Bush-bashers on fiscal policy coming around to give Obama some of the credit he is due: EconomistMom now calls the "Bush tax cuts" the "Bush-Obama tax cuts".

Supreme Court justice nominee Sotomayor's decisions affecting baseball and football get a look from The Sports Economist.

The world's first transparent (as in "glass walled, you can see through it") auto factory, via Carpe Diem.

"The late" fiscal stimulus, reviewed by Keith Hennessey. "CBO says that $25 B of spending had gone into the economy by May 22nd. That’s less than 4% ..."

How the "public option" government health plan to be included in Obama's national health care proposal, purportedly simply as an extra free choice option for consumers, is likely to be a camel's snout sneaking forward through tent in the dark of night with a knife in its mouth to murder private sector health care in its bed, explained by Greg Mankiw.

How wrong Nobel economists can be. This time Joe Stiglitz (not Krugman). Back at the end of March, Stiglitz was publicly savaging the Treasury's "Public Private Investment Program", intended to get investors to buy troubled assets from banks, as a give away that could give a 50% return to investors at the cost of a -40% return to the government. But, as it turned out, the plan hasn't been able to attract investors. So either a 50% return isn't attractive to them or Joe was pretty darn wrong, says Falkenblog.

"French courts are basically legislating Reality TV shows [as we know them at least] out of existence by stipulating that they pay overtime and provide holidays as well as allowing contestants to sue for unfair dismissal..." [Oxonomics, HT: AdamSmith.org]

The decision that Washington should save Detroit was made for Obama by...

a not-quite graduate of Yale Law School who had never set foot in an automotive assembly plant ... when the administration was divided over whether to support Fiat’s bid to take over much of Chrysler, it was Mr. Deese who spoke out strongly against simply letting the company go into liquidation, according to several people who were present for the debate... [NY Times, HT:Flyinderthebridge]

The asking price for Pol Pot's toilet (and a few accessories) is $1.5 million, reports Marginal Revolution. (One wonders what the price would be for Eva-and-Adolph's bidet.)

Friday, June 05, 2009

If you wanted to know whether there is life on a planet, what would you look for?

Scientists have located emperor penguin breeding colonies in Antarctica after spotting giant poo stains from space. Satellite images picked up huge red-brown stains on the pristine white sea ice, indicating the presence of thousands of penguins ...

Peter Fretwell, co-author of the study and geographic information officer at British Antarctic Survey, said his chance discovery would revolutionise the way scientists monitored penguins ... [Ananova]

Physicists scientifically disprove ghosts and vampires. (The Hollywood model of them at least.)

Civil right for lab rats?* Will this be their savior?

[* free version for non-WSJ subscribers]

Strange video chemistry, European style.

Thursday, June 04, 2009

There's much talk and debate of late about projections showing that rising health care costs pose a very real threat both to the finances of the government and the viability of the the economy in years to come -- years that are getting closer to now, well, every year!

And if you look for the reasons why the cost of health care has been growing at a faster rate than the economy for two generations now, you will find many experts saying that Reason #1 is the development of expensive new medical technologies. Broadly defined, these range from high-tech hospital equipment to prescription drugs to behavioral therapies developed through costly clinical trials and directed by skilled professionals.

For instance, a CBO paper on the subject [.pdf] states...

most analysts have concluded that the bulk of the long-term rise [in cost] has resulted from the health care system’s use of new medical services that were made possible by technological advances, or what some analysts term the “increased capabilities of medicine.”... and cites estimates of the post-1965 increase in health care costs as being from 38% to >65% attributable to the cost of new technology.

Yet to many persons who think "economically" something about this seems amiss. After all everywhere else in the economy improvements in technology reduce cost.

Advances in technology by definition increase productivity, to provide more for less. The horse and carriage became the automobile because the latter provided better transportation service at less cost, and the Model T became today's vehicles with On Star (as long as GM lasts) air conditioning and stereo satellite radio for the same reason. The computers themselves used in medical technologies cost less and less for the computing power they provide each year.

So why is it that only in health care new technology increases cost? This disparity leads a good number of people to conclude that either there is some economic "paradox" affecting the health care sector of the economy, or something very wrong is at a work -- such as special interest groups lining their own pockets by driving patients to less effective, more costly medical interventions.

But in fact there is no paradox to explain. Technological advances work in the health sector just as everywhere else, enhancing productivity continually, making new services available for the first time and improving the cost-benefit ratio of existing services.

Thirty years ago, my father had a cataract operation that was performed with a blade, and afterward he had to lay in a hospital bed for days with his head secured to keep it from moving. Recently my mother had a double cataract operation and it was walk-in, walk-out, "I can see again!" Hip and other joint replacements today are performed in the hundreds of thousands annually, two generations ago they were an impossibility. Studies of new prescription drugs show they provide large cost-benefit gains in averting expensive interventions (for heart attacks, strokes, etc. ... not to mention burial costs) that would be expected without their use.

So, if medical technology is providing large cost-benefit gains, just like technology in all other parts of the economy, we are still left with the question as to why it is the only kind of technology that increases cost to consumers rather than reduce it.

The first part of the answer is that the simple creation of a new technology increases its cost to the economy -- a service that doesn't exist costs zero, so the cost of that service once it does exist is an increase. As ever more new medical technologies come into existence, their aggregate cost as a portion of GDP steadily rises.

But of course that's not the total answer because the same thing is true of other technologies -- the cost of computing technology comprises a significant portion of GDP today, compared to about zero 60 years ago, yet nobody is complaining about "the ever rising cost of computers to society".

The second, big, part of the answer is that most other major technologies are developed primarily for use in commerce, so their use produces a financial return that pays for the use ... making investment in the technology self-funding. For instance, computer users from Fortune 500 corporations to freelance writers increase their net revenue by using computers, and the resulting increase in their income pays the money cost of their computers ... and also pretty much pays for the entire computer industry's research and development costs for new products and technologies.

Indeed, the requirement that the business user's purchase of a computer pay for itself financially imposes a strict spending constraint on purchases, and directs the computing industry's investments in new technoligies towards those that will pay for themselves, monetarily.

Here is where medical technology is very different. With medical technologies the payoff to the final consumer, while it may be large and extremely valuable, is non-monetary. It doesn't produce revenue for the user. So the monetary cost of the consumer's use of the technology has to come from somewhere else: from savings ... or from reduced consumption on lifestyle, clothing, food ... or from other people, such as all the other persons who pay premiums to the same insurer, and from taxpayers.

Moreover, because the payoff from medical technologies can indeed be very large to consumers -- the difference between years of living in comfort and living years in pain, or not living at all -- demand for them can be very high. If you happen to buy a computer or car totally for personal, non-revenue generating use, you will weigh its recreational value to you against the value of other things in your life, and limit your expenditure on it accordingly. But if you are talking about a technological medical procedure that will be the difference between you (or a loved one) having a high-quality life or low-quality life for many years to come ... or no life at all! -- well, you gotta have it! If your savings and income aren't enough to pay for it, you are going to want your co-insureds and fellow taxpayers to pay for it. "Pony up!"

And that's why advances in medical technology drive increases in the cost of health care to consumers, while technological advances everywhere else in the economy reduce costs to consumers. (1) The cost of medical technology is not financially, monetarily, self-funded from the productivity gains it produces, as is the cost of technologies developed for use in business and commerce; compounded by (2) The demand for such technologies can be extraordinarily high, driving up its cost -- especially when that price is to be paid by others, unconstrained by the consumer's own income and savings.

Is there a remedy for this? More, later ...

Wednesday, June 03, 2009

Or: "Cap and trade" becomes "Pork out and squeal."

The "cap and trade" plan to reduce atmospheric carbon emissions by industry, to fend off global warming, is intended to work through a permit system that enables permit holders to emit given amounts of CO2, but limit the total amount emitted.

Firms are to be able to trade permits in a market, so that the businesses that most need permits can buy them, while those able to most efficiently reduce their emissions can profit from doing so (by selling permits) giving them an incentive to do so. The whole process can be much more economically efficient than governmental rationing of the right to emit. In theory.

But the first critical question is: how are permits to be distributed?

The starting-point idea behind the whole concept of "cap and trade" is that permits will be auctioned off by the government. Then an efficient market in them is created right away, as the firms that need them most bid the most for them, they are distributed efficiently through the bidding process, and market prices are quickly established.

Well, considering that idea for a moment, you may think that the money to be received by the government from the auction actually is a tax -- and you'd be right!

Of course, it is a tax. How do you reduce the production of something? By increasing the cost of production. The amount that businesses must pay to the government through the auction process for permission to emit CO2 into the atmosphere is a tax on such emissions that increases the cost of emitting, and so reduces their amount.

Will that tax be passed on by businesses to consumers? Of course it will, to the extent that businesses can pass it on. That's what will reduce "consumer demand" for CO2 emissions. If you want to reduce CO2 to fight global warming, this is a good thing.

Even if you are a "small government" type who doesn't want to see the government collect more tax revenue, this can still be a good thing -- because the government can remit the tax collected back to taxpayers by reducing other taxes, such as income taxes, payroll taxes, whatever ... and this "Pigouvian tax" on emissions is less distorting to the economy than the other taxes it would replace as explained in in Greg Mankiw's Pigou Club Manifesto. So the net tax collected could be zero -- with the tax system's distortion of the economy actually reduced in the process.

At worst (if more realistically) this "auction tax" would reduce the need to increase other taxes in our era of ever-rising deficits (a need that will soon arrive big time) and this Pigovian tax would be much less harmful to the economy than other kinds of tax hikes, such as big increases in the income tax, or a new national sales tax.

But now you may think, well, if this whole cap-and-trade business boils down to really being a tax on CO2 emissions, wouldn't it be a whole lot simpler just to tax CO2 emissions themselves, directly, to achieve the same thing?

The answer to which is "yes" -- you'd be right again! As Professor Mankiw says: "a cap-and-trade system is equivalent to a tax on carbon emissions" -- that is, when it is done right, it is.

But what if it is done wrong? What if, for instance, politics intervenes so the emission permits aren't auctioned off, but instead are handed out by politicians for free to their friends, campaign contributors, and the constituents they want to win over before the next election -- distributed in accord not with economic efficiency but political influence?

Then the whole system starts going wrong. The permit system that reduces CO2 emissions still increases cost to consumers -- but instead of the "tax" that consumers pay through higher prices going to the government, it goes to ... the producers of CO2 emissions!

Let President Obama himself tell you himself (while speaking to the Business Roundtable, this past March 12):

Now, the experience of a cap and trade system thus far is that if you’re giving away carbon permits for free, then basically you’re not really pricing the thing and it doesn’t work -- or people can game the system in so many ways that it’s not creating the incentive structures that we’re looking for.Obama's budget director, Peter Orszag, until recently the head of the Congressional Budget Office, explains what "gaming the system" means...

"If you didn't auction the permit, it would represent the largest corporate welfare program that has ever been enacted in the history of the United States.Last year, a report [.pdf] by Orszag's CBO provided more detail...

"In particular, all of the evidence suggests that what would occur is the corporate profits would increase by approximately the value of the permit.

"So that -- whatever that is, $600 billion, $800 billion, whatever the value is, would go in a sense almost directly into corporate profits rather than being available to fund energy efficiency investments and to provide a cushion or some compensation to American households.

"That is why the president, I think, has made absolutely the right choice in saying that the permit should be auctioned"